A multi-product approach

reactant based h2 production & the future of the hydrogen economy

Download to Read Offline

Table of Contents

- The State of The Hydrogen Industry

- Technologies for Low and Zero Emissions Hydrogen Production

- A Novel Approach: Reactant Based Hydrogen Production

- Advanced Ceramic Co-Products

- Risks and Limitations of Reactant Based Hydrogen Production

- Likely Applications for Reactant Based Hydrogen Production

- Conclusion

The State of the Hydrogen Industry

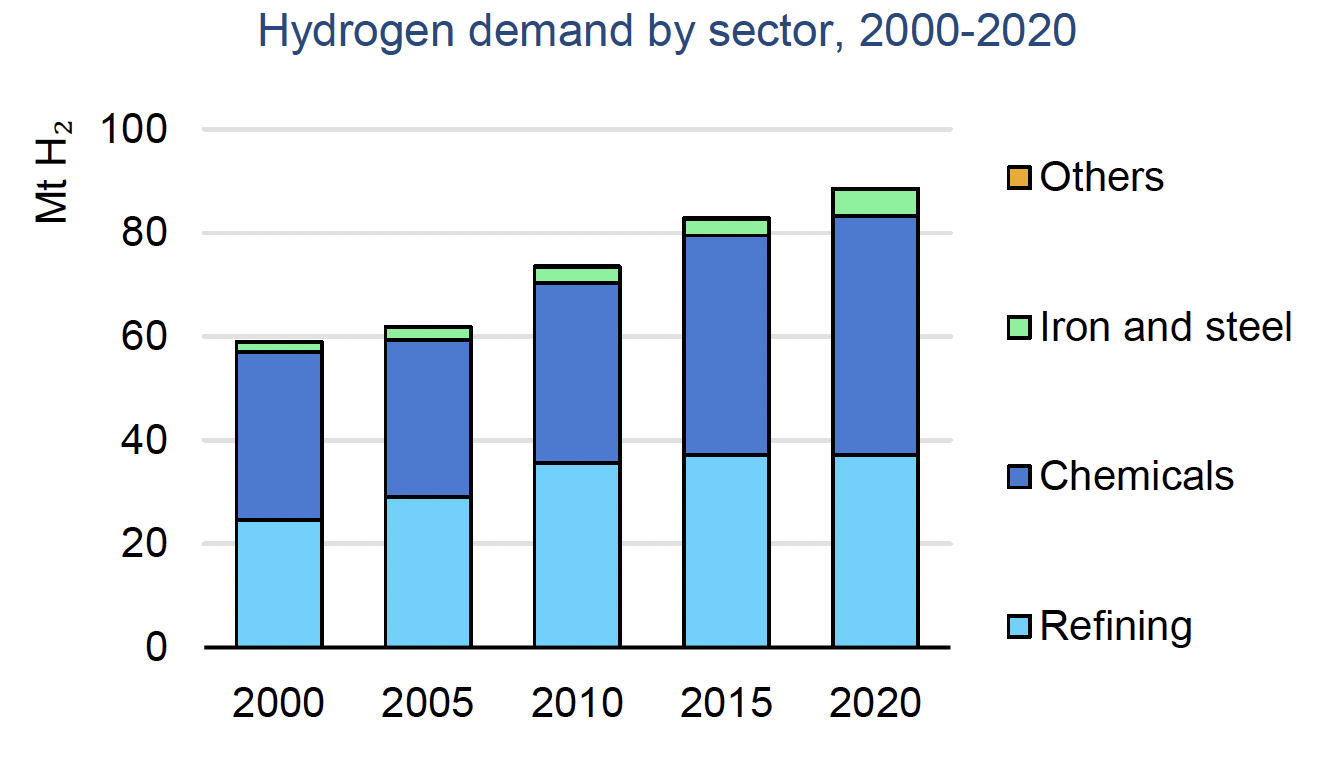

Hydrogen is a vital commodity and is necessary to the function of multiple global markets. In 2020, hydrogen demand reached 90 million tons, and this demand is steadily rising, having risen by almost 50% in the past 20 years. The major consumers of hydrogen are in the industrial sector, where refineries consume nearly 40 million tons, and the combined consumption of ammonia and methanol production comes in at 45 million tons.1

Industries That Require Hydrogen

The future of hydrogen is going to be heavily shaped by the demand from industries that require hydrogen for their production processes. As stated above, the primary consumers of hydrogen are refineries, ammonia, and methanol. Refineries use hydrogen to lower the sulfur content in diesel fuel, which has increased in demand globally. This makes refineries currently the largest consumer of hydrogen, although this is expected to change as the transition to lower and zero-emissions vehicles continues.

Ammonia (NH3) and methanol (CH3OH) are expected to see increased demand, which means that hydrogen demand from the ammonia and methanol industries will increase as well since hydrogen is a primary feedstock in the production process. Ammonia and methanol are also seen as carriers of hydrogen, since pure hydrogen is difficult to transport, while ammonia and methanol are relatively easy to store and transport over long distances. Methods for separation of hydrogen from these chemicals — or even configuring vehicles to use ammonia or methanol directly as a fuel source — means that demand for these chemicals may expand beyond their current industrial uses.

Outlook for Industrial Hydrogen Demand

Hydrogen for industrial uses is expected to exceed current industrial demand, not just from ammonia and methanol production, but also from steel and cement production. Currently, steel and cement production requires high heat stages that use carbon-based fuels as the primary heating method. As these industries look to decarbonize their production processes, hydrogen is considered the fuel of choice. As steel and cement production see increased adoption of hydrogen as a fuel, the demand for hydrogen in these sectors will be significant.

Hydrogen and Emissions

While hydrogen itself is considered a green, renewable resource, current hydrogen production is highly carbon-intensive. The primary method for hydrogen production is known as steam methane reforming (SMR). This process reacts natural gas and steam to create carbon dioxide and hydrogen. The gases are separated to get the high purity hydrogen required for industrial use. SMR results in large amounts of carbon dioxide, with approximately 830 million tons of carbon dioxide emissions every year resulting from hydrogen production.2

For this reason, there are several categories of hydrogen in relation to the emissions resulting from the production processes. The three primary categories are grey, blue, and green hydrogen. Grey hydrogen is produced using SMR. Blue hydrogen is also produced using SMR but has a carbon capture, utilization, and storage (CCUS) system. Green hydrogen is any hydrogen production method that results in zero emissions.

Have a question about our technology or company? Ask us anything!

Technologies for Low and Zero Emissions Hydrogen Production

Blue Hydrogen and Carbon Capture

Hydrogen production via SMR with CCUS was long hailed as the best way to transition to a larger hydrogen economy, creating the infrastructure and demand for hydrogen, while also buying time for green hydrogen production to scale and come down in price. CCUS systems typically aim to be 90% effective at capturing carbon released in the SMR process.3 While this is lower carbon dioxide emissions than SMR without CCUS, the remaining 10% would still be the equivalent of more than 80 million tons of carbon dioxide emissions a year if all SMR plants added carbon capture.

There is also the difficulty of sequestration with carbon capture technology. The captured carbon dioxide needs to be stored in a way that will ensure it does not get released. A common approach to this is to store hydrogen underground. However, this has resulted in land tremors in regions where carbon is sequestered deep underground, and if the carbon does leak back to the surface it could be catastrophic for the local environment.

Electrolysis

Considered to be the future of hydrogen production, electrolysis runs electrical currents through water, or a water-based solution, to produce hydrogen. There are two types of electrolyzers: alkaline, and polymer electrolyte membrane (PEM). Alkaline electrolysis utilizes an electrolyte solution, while PEM electrolyzers use a specialized barrier that only allows positively charged hydrogen to pass through after it has been split from water by an electrical current. After passing through the membrane the positively charged hydrogen receives an electron and forms H2 gas.

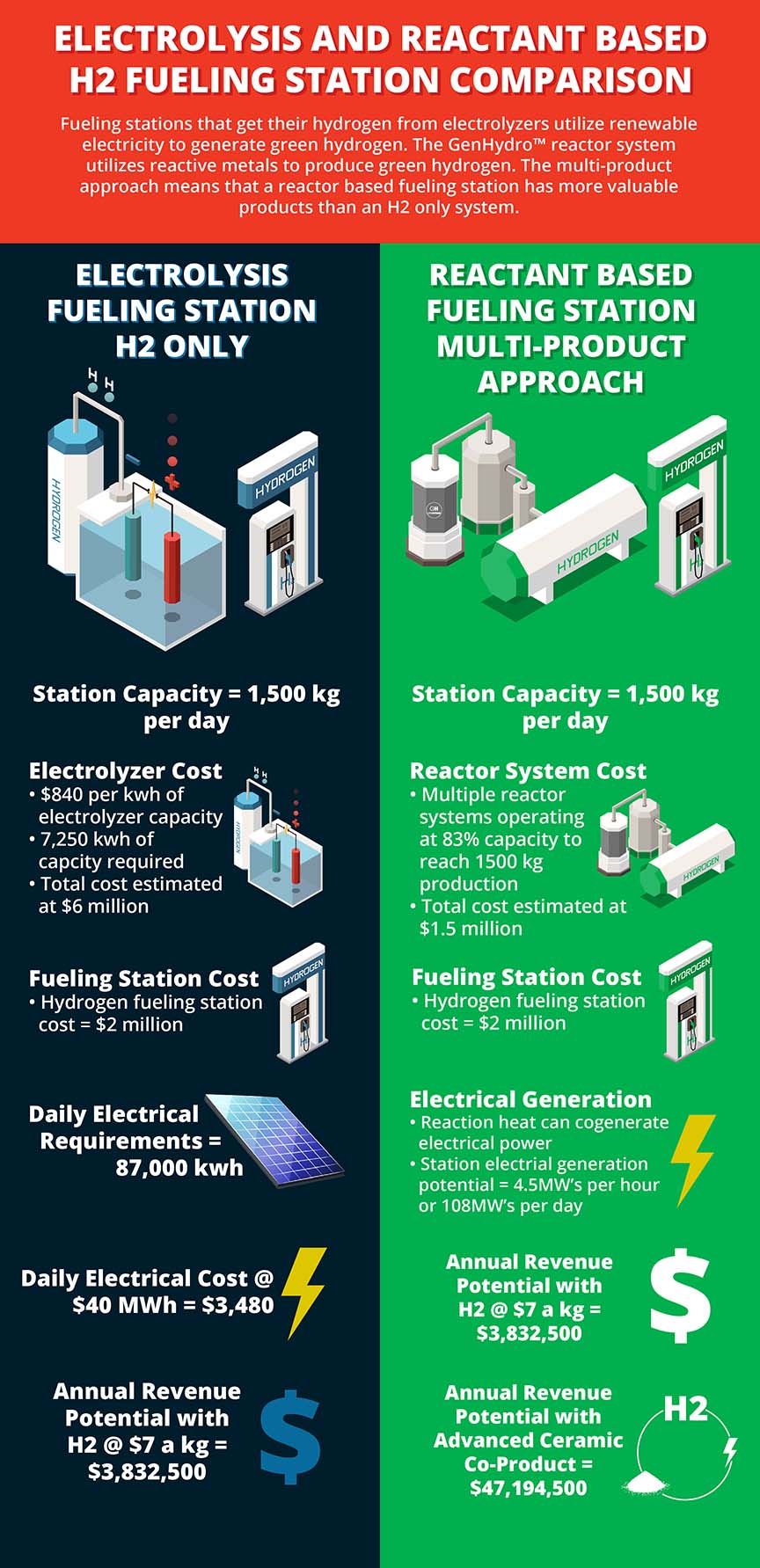

Electrolysis is an effective way for hydrogen production and is expected to be the dominant method of a decarbonized future. Electrolysis does face several obstacles, however. The manufacturing cost for electrolyzers is currently quite high, with CapEx for both alkaline and PEM electrolyzers exceeding $1,000(USD) per kW of capacity. This puts 10MW of electrolyzer capacity, capable of about five tons per day of hydrogen production, at $10 million. The Energy Transitions Commission estimates that it will cost $15 trillion to have the electrolyzer capacity necessary to meet the demand of the hydrogen economy.

Additionally, if electrolysis is to be considered zero emissions, it must use a renewable source for electricity generation, such as solar, wind, or hydro dam. Given limited hydro dam availability, the increase in solar and wind to generate enough power to cover hydrogen production requirements is also going to be a tremendous investment. The Energy Transitions Commission estimates that the additional power requirements for hydrogen production will reach about 30,000 terawatt-hours by 2050. That is more than global electrical power consumption in 2019. That is also in addition to the estimated 90,000 terawatt-hours of renewable energy required for the electrification of sectors that will not use hydrogen.4

Methane Pyrolysis

A fairly new method for hydrogen production from natural gas is known as methane pyrolysis. This method uses a high-temperature separation of methane in a zero-oxygen environment, resulting in hydrogen production and a solid carbon byproduct. Methane pyrolysis is considered a green method of hydrogen production since the carbon is not released but is instead collected as a solid product that can be sold into various markets.

The limiting factor for methane pyrolysis is the market for solid carbon products. The ability to sell the solid carbon allows the hydrogen to be sold at a low cost. While the solid carbon market is large, it is not large enough to allow methane pyrolysis to scale hydrogen production to meet current demand.

A Potential End to Natural Gas

Another limiting factor for methane pyrolysis and SMR with CCUS is the fact that it uses natural gas sourced from drilling. Multiple studies have shown that 2-6% of captured methane from drilling is leaked into the atmosphere at the drilling site. This has resulted in dramatic increases in methane released into the atmosphere over the past 10 years, corresponding with rapid expansion in natural gas adoption. One study estimated that 544,000 tons of methane are released from drilling sites in Texas, which is the equivalent of 46 million tons of carbon dioxide.5 For this reason, scientists and policymakers are becoming increasingly suspicious of natural gas as a transition fuel, let alone a long-term solution for hydrogen production.

A Novel Approach: Reactant Based Hydrogen Production

A hydrogen production method that has been explored but has yet to reach commercialization is known as reactant-based hydrogen production. This method has been explored by the U.S. DOE6, MIT7, as well as others, and is continuing to be explored by academic institutions as a potential solution to emissions-free hydrogen production. The primary barrier to scaling this approach has typically been associated with feedstock cost. However, like the methane pyrolysis approach, the sale of the byproduct will more than cover the cost of the feedstock, allowing for a profitable solution to emissions-free hydrogen production.

Types of Reactant Based Methods

While several approaches to reactant-based hydrogen production have been explored, they typically fall into two categories: promoter method, and hydrothermal method. The main differences in these approaches being the use of a catalyst promoter for initiating the reaction or using heat and pressure to reduce or completely eliminate the need for a promoter compound.

Promoter Method

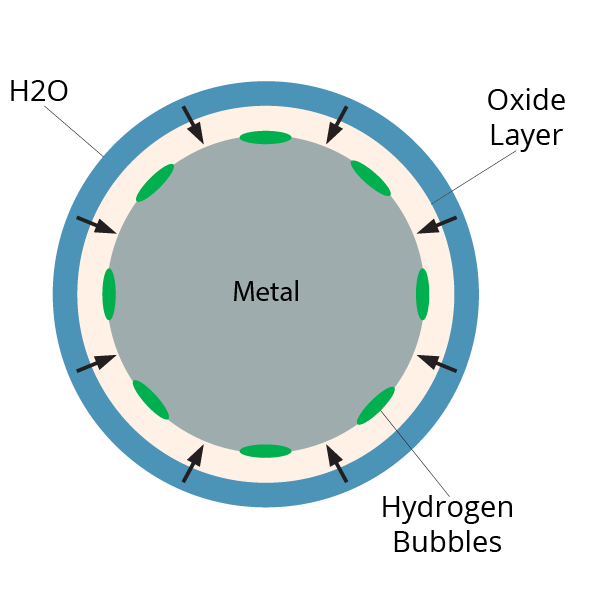

The promoter method is the most explored reactant-based approach to date. There are several elements that are reactive in the presence of water or steam. These mostly metallic elements will typically form an oxide layer when exposed to air, or a hydroxide layer when exposed to water. The formation of this layer in the presence of water consists of the metal attracting hydrogen and oxygen to itself, forming a hydroxide, while any remainder of hydrogen gets released as a gas. What a chemical promoter will do is continuously remove the reacted layer, repeatedly exposing the metal surface, thus sustaining the reaction until the metal has converted completely to a hydroxide material.

Hydrothermal Method

The end goal of the hydrothermal method is the same as the promoter method, except the hydrothermal method uses high heat and pressure to initiate the reaction instead of a promoter. The reaction is exothermic, meaning it releases heat, so the reaction will sustain itself until completion. High heat and pressure steam continuously remove the oxidized layer of the metal, while simultaneously reacting with the exposed metal to release hydrogen gas until the metal has completely reacted.

Cogeneration

Being that the reaction of both the promoter and hydrothermal methods are exothermic, there is potential for cogeneration of usable energy. At a smaller scale, promoter-based reactors are capable of producing enough heat energy to be used for heating water or forced air heating. Larger scale systems have the potential for cogenerating significant amounts of electrical power. By injecting additional water, excess steam is produced in the reaction process, which can be run through a steam turbine. Multiple system outputs can be combined, allowing for larger turbine operation, ultimately with the potential of utility-scale power capacity.

Reactive Metals as A Portable Fuel

A major benefit that reactant-based methods have over other forms of hydrogen production is the portability of the fuel. Metals are easy to transport, which means that these systems can be constructed in remote areas that don’t have easy access to other fuel sources, and can’t easily construct solar or wind capacity. Certain operations, such as mining, can benefit from on-site hydrogen production that is dependent on nothing more than the ability to transport a reactive metal to serve as the fuel for hydrogen production and even cogenerated power. Hydrogen can be used in these instances for added power generation by means of a PEM, or for fueling mining vehicles. This easy portability of the fuel source means that hydrogen can be made available virtually anywhere on earth that a reactor can be installed, eliminating the need to transport hydrogen over long distances.

Advanced Ceramic Co-Products

Both the promoter and hydrothermal methods for hydrogen production result in a byproduct. This byproduct is a metal oxide powder, which is considered an advanced ceramic material. The properties of this material make it valuable for several applications, with uses in existing markets valued in the billions of dollars.

What Are Advanced Ceramics?

Advanced ceramics are high purity metal oxides that have properties such as high hardness, high heat conductivity, and high melting points. These characteristics make them optimal for applications where durability under extreme conditions is important. Advanced ceramic powders are used in applications ranging from electronics, cutting tools, orthopedic implants, automobile and aviation parts, and abrasives. They can also be used in filtration, and catalyst supports.

Major Advanced Ceramic Markets

|

• Electronics (Microelectronics, insulators, sodium vapor lamps) |

• Structural (Cutting tool inserts, abrasives, corrosion-resistant parts) |

|

• Thermal spray (thermal barriers, corrosion resistance) |

• Semiconductor and microchip polishing (CMP slurry) |

|

• Ceramic arc tubes |

• Medical (orthopedic implants) |

|

• Filters (water filtration, adsorption) |

• Auto catalyst coatings |

|

• Catalyst support (hydro-processing) |

Growing and Emerging Applications

Growing applications for advanced ceramics are in the development of products such as sapphire or high-performance glass. Production costs for sapphire glass are currently high, but as more applications arise and production is scaled, the price is coming down and sapphire glass is making its way into more and more consumer products. Corning’s Gorilla Glass is an example of a high-performance glass product that utilizes metal oxide powders as part of the raw material in its production process.

Advanced ceramics are finding increased interest in the construction industry as well, as advanced ceramics can help create highly durable, long-lasting materials that would be optimal for certain construction applications. As research continues in ceramic materials manufacturing, the potential for ceramics to serve as the material for applications where plastics and metals are used is growing, meaning the future for advanced ceramic materials is expected to be one of continued and rapid growth.

Nano-Ceramic Powders

A sub-category of advanced ceramics is nano-ceramic powders. These are ceramic powders with a particle size of 100 nanometers or less. The largest market for these powders is currently in the electronics and microelectronics industries. A rapidly growing application is chemical mechanical planarization (CMP). This application of nano-ceramics uses the powders in a liquid slurry for the purpose of precise polishing of semiconductors and microchips. The nano-particles allow for achieving blemish-free surfaces on incredibly thin and small parts. This has been a major enabler for developing microchips that are increasingly smaller.

the electronics and microelectronics industries. A rapidly growing application is chemical mechanical planarization (CMP). This application of nano-ceramics uses the powders in a liquid slurry for the purpose of precise polishing of semiconductors and microchips. The nano-particles allow for achieving blemish-free surfaces on incredibly thin and small parts. This has been a major enabler for developing microchips that are increasingly smaller.

Ongoing research in nano-ceramics is leading to discoveries for additional applications. Sintered ceramics made using nano-powders had a level of plasticity, meaning these materials can potentially bend to a certain degree without breaking, a property that other ceramics do not have.

Market Size and Value of Advanced Ceramics

The market size for advanced ceramics is multiple billions of dollars. Depending on the purity and particle size, an advanced ceramic powder can be priced between $5 per kg to over $50 per kg. Nano-particle ceramic powders that are also high purity are valued significantly higher than micron-sized particles of the same material and purity. A hydrogen plant that utilizes a reactant-based approach does not need to seek the highest possible value for the resulting advanced ceramic powder in order to be profitable. This means that these powders can be sold at a competitive price, allowing for a pathway to rapid acquisition of market share. This may also have an effect of expanding the advanced ceramics market as price is often the barrier to manufacturers using advanced ceramics in their products.

Risks and Limitations of Reactant Based Hydrogen Production

While the theoretical limit to reactant-based hydrogen production is quite high, the true limiters of this approach are of a logistical and market nature. More specifically, the ability to acquire the feedstock and the ability to sell the advanced ceramic co-product are the major considerations when determining a feasible plant size.

Feedstock Availability

The feedstock for reactant-based hydrogen production is plentiful, being that it is available in millions of tons per year. These metals can be purchased new or as recovered scrap material. The recovered scrap material lowers the overall energy intensity of the feedstock since using it for hydrogen production would be extending the material lifecycle and using it to put energy back into the economy. While the feedstock is available in the millions of tons as scrap material, the ability to acquire it in large amounts may be a logistical challenge and may prove to be a limiting factor in hydrogen production capacity.

Co-Product Sales

The more significant limiting factor will be the ability to sell the co-product to ensure the greatest potential of plant profitability. This will require competing with existing suppliers of the material, but this approach does have the advantage of being able to offer lower pricing than existing suppliers while still being highly profitable. Ultimately, the market size and ability to acquire market share will be the deciding cap for plant production. This is similar to the limiting factor of methane pyrolysis, which also has an advanced material co-product (carbon black, graphene, and others), the sale of which is necessary to overall plant profitability.

Even with this limitation, a reactant-based hydrogen plant can easily exceed the current green hydrogen production capacity of some of the largest plants in existence, and still have space to grow significantly. A five metric ton per day hydrogen plant utilizing a reactant-based method would only produce enough advanced ceramic material in a year to take up a few percentage points of market share. This means that the limitation of plant size is quite high, even if the advanced ceramics market doesn’t continue on its current trajectory of significant growth.

Likely Applications for Reactant Based Hydrogen Production

The application for this technology covers a range of industries where hydrogen is in demand. A large enough production facility could provide enough hydrogen for an ammonia or methanol plant, for which there is incredible interest among ammonia and methanol producers eager to decarbonize. This method can also be used to decarbonize natural gas by means of hydrogen blending into natural gas pipelines, and it can be used for providing a significant amount of hydrogen for fueling stations serving commercial or passenger fuel cell vehicles. This approach can also produce enough hydrogen to assist steel or cement manufacturers in decarbonizing by using hydrogen instead of carbon-based fuels.

Conclusion

If a zero-emissions hydrogen economy is going to be realized, reliance upon SMR with carbon capture is not the best way forward, since reliance upon natural gas will always mean significant methane emissions from drilling sites, and carbon capture is not 100% effective. Methane pyrolysis, also being dependent on natural gas means that drilling site emissions will continue if natural gas is needed at scale. Electrolysis will and is playing a significant role, but the increase in the renewable infrastructure necessary for electrolysis to meet hydrogen demand is massive, and the current trend of electrolyzer capacity installation is not enough to meet 2030 or 2050 targets.

Reactant-based methods for hydrogen production can start to provide green hydrogen now, without large renewable energy requirements. The largest electrolyzer plants have a hydrogen production capacity ranging from 5-10 tons of hydrogen per day and have required large solar installations. A reactant-based plant can exceed that production capacity with a smaller overall footprint since this approach does not require large solar or wind installation.

The future of hydrogen production is likely to be a blend of production methods. No single method will be able to meet global demand on its own, especially not in the timeframe needed to reach emissions reduction goals. A combination of approaches that includes reactant methods is going to be vital to hitting green hydrogen production targets and doing so in an affordable and sensible way.

References

- (2021, October). Global Hydrogen Review 2021 – analysis. IEA. Retrieved from https://www.iea.org/reports/global-hydrogen-review-2021.

- (2019, June). The future of hydrogen – analysis. IEA. Retrieved from https://www.iea.org/reports/the-future-of-hydrogen.

- Moseman, A. (n.d.). How efficient is carbon capture and storage? MIT Climate Portal. Retrieved from https://climate.mit.edu/ask-mit/how-efficient-carbon-capture-and-storage.

- Making the hydrogen economy possible: Accelerating clean hydrogen in an electrified economy. Energy Transitions Commission. (2021, June 2). Retrieved from https://www.energy-transitions.org/publications/making-clean-hydrogen-possible/.

- Borunda, A. (2021, May 3). Natural gas is a much ‘dirtier’ energy source, carbon-wise, than we thought. Science. Retrieved from https://www.nationalgeographic.com/science/article/super-potent-methane-in-atmosphere-oil-gas-drilling-ice-cores?.

- Petrovic, J., & Thomas, G. (2008). Reaction of aluminum with water to produce hydrogen. energy.gov. Retrieved from https://www1.eere.energy.gov/hydrogenandfuelcells/pdfs/aluminium_water_hydrogen.pdf.

- Stauffer, N. W. (2021, June 3). Using aluminum and water to make clean hydrogen fuel-when and where it’s needed. MIT ei. Retrieved from https://energy.mit.edu/news/using-aluminum-and-water-to-make-clean-hydrogen-fuel-when-and-where-its-needed/.